Eight reasons to be optimistic about 2019

Happy New Year to all and I hope that you all had a wonderful and peaceful holiday season. As I noted in my recent quarterly performance report, we remain optimistic about the markets over the long-term but have a cautious short-term outlook as we expect volatility to remain with us for the foreseeable future.

It is not all doom and gloom as the papers would lead you to believe. There are still many positive fundamentals such as a positive premium for investing in shares over the long-term, company earnings expected to be around 10% for the current year and still positive GDP growth, (albeit slowing).

As the news tends to focus on just the negatives, I decided to highlight some of the positives and found this recent article by New Zealand portfolio manager Richard Stubbs from Castle Point Funds Management.

Eight Reasons to be optimistic about 2019

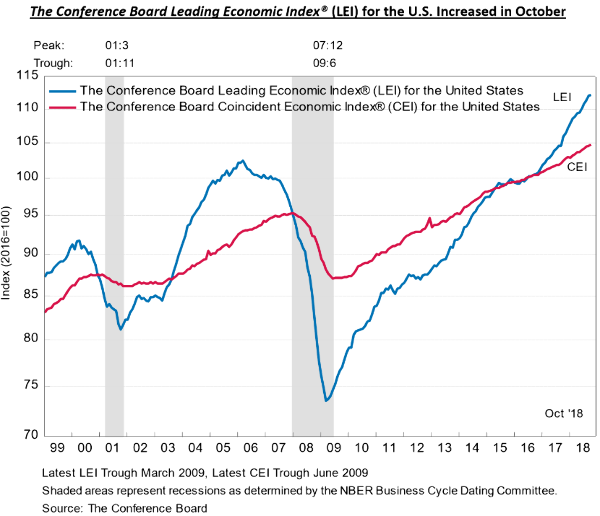

1. Ambiguous US economic data

There is plenty of discussion around whether the US is approaching a recession. However, recession indicators are far from aligned. As an example, since the 1950s, a turn-down in the Conference Board Leading Economic Index has been a very reliable indicator of an oncoming recession, peaking on average 6-8 months before. There is currently no sign of that yet.

2. Reserve Bank easing is not necessarily over

Much of the negative narrative around markets is around the end of central bank easing. However, this will only occur if economies remain strong. Any further weakening of economic data is likely to result in far more dovish outlook statements from central banks. Another quarter point hike by the New York Federal Reserve Bank in December was virtually a given a few months ago, with follow-through expected in continued tightening in 2019. Recent rhetoric has been far more dovish. And while inflation remains benign further tranches of quantitative easing are not off the table.

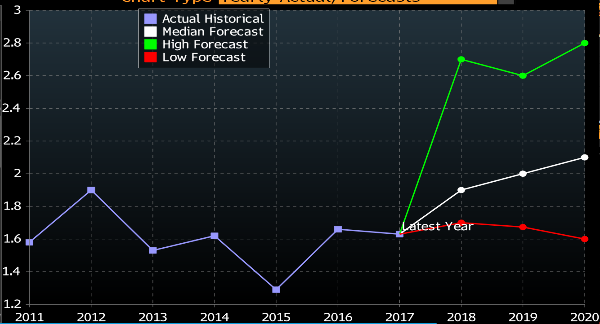

3. No sign of inflation

In our opinion this bull market will be well and truly over when inflation expectations rise, but there remains little evidence that this is a near-term threat. Headline inflation expectations are falling as a result of the drop in the oil price. While inflation remains benign, rate cuts and QE (quantitative easing – i.e. stimulus) can be pulled out again should any real signs of economic weakness arise. However, once core inflation kicks in, these tools will be removed from use for the foreseeable future. In our opinion, increasing core inflation remains as the greatest risk for ending this bull market.

US Core CPI Actual and Forecasts

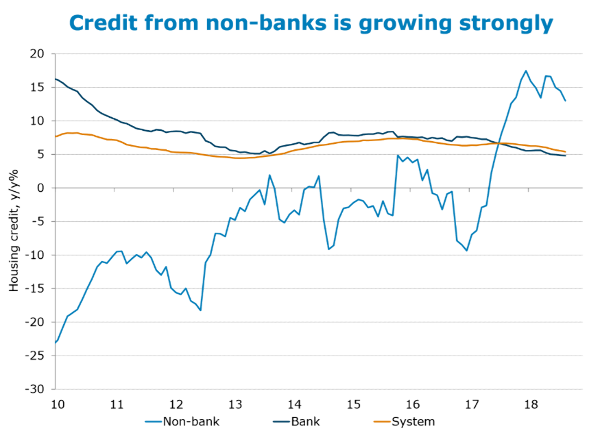

4. Australian property declines appear to be driven by a tightening of credit, which is almost over

Nearer to home there is concern about what the decline in Australian property prices might mean and whether the recent softness in Sydney and Melbourne prices will spread to New Zealand. If the downturn was caused by rising interest rates or deteriorating household finances, making mortgage payments difficult, there would be concern it could become a re-enforcing downward spiral. However, the price weakness has been caused by the banks wanting to reduce their exposure to high-end property prices in Sydney and Melbourne, making mortgages harder to get, not harder to service. There is no evidence that it is creating any systemic risk to Australia’s economy - unemployment remains low, commodity prices stable, and a large infrastructure spend is on the horizon. Non-bank lending is surging to fill the gap left by the mainstream banks.

Source: ANZ

5. There is still value

There will always be companies that are out-of-favour with the market due to poor recent performance. Finding these companies and holding them for a long-enough period to allow them to recover is a proven investment strategy. Further, these companies have not participated in the strong market rally over recent years so should not be as vulnerable to a market sell-off.

6. There is still quality

In a 2005 memorandum by the late Sir John Templeton, who accurately foresaw the pending financial crisis, he gave his opinion on how to invest through it.

“Not yet have I found any better method to prosper during the future financial chaos, which is likely to last many years, than to keep your net worth in shares of those corporations that have proven to have the widest profit margins and the most rapidly increasing profits. Earning power is likely to continue to be valuable, especially if diversified among many nations.”

Market volatility just means you get to buy these companies more cheaply.

7. There is still cash on the side-lines

If this is the end of the bull market it will have been the best forecasted. Prior to this market correction there were plenty of news articles forecasting its arrival and plenty of professional and private investors appear to have been relatively defensively positioned. That is not an orthodox end to a bull market, which is usually preceded by euphoria. There does not appear to be any systemic leveraged investment into equity markets that is often the cause for the crash.

8. The sun will come up

It is a well-documented psychological bias that our emotions are heavily affected by near-term events. In our investing lifetime we have witnessed the ‘87 crash, the Asia crisis, the Dot.com bubble and the Global Financial Crisis, and many market corrections in between. Those times often felt horrible, but the world kept on turning, the sun kept coming up and they were surprisingly quickly forgotten. Provided you don't put yourself in position where you risk suffering total loss of capital over those times, wealth can be amassed over a long period that includes them.

Conclusion

It is critical that you know what your investment horizon is. If you are planning to cash in part or all your portfolio to buy a home soon, then you have a very short-term investment horizon and should not be invested in a long-term portfolio, (i.e. a growth portfolio).

My view is that if you have a long-term investment horizon, you have the luxury of not worrying about the short-term noise and volatility. It does not matter who the prime minister is, who the American president is, or which party is in power. What you do need to do, is stick to your investment or retirement plan.

If you are not sure what your investment horizon is or are planning on making a large purchase, then you should speak about this with your financial adviser, that is what they are there for.

As always, if you have any questions on this or any financial matter, please contact your financial adviser.

Article by Joe Byrne, BA, AFA - Read More

Disclaimer: This article has been prepared for the purpose of providing general information, without taking into consideration any particular investor’s objectives, financial situation or needs. Any opinions contained in it are held as at the report date and are subject to change without notice. This document is solely for the use of the party to whom it is provided.

Maximising Rental Cash Flow: Is Fortnightly Better Than Monthly?

A common request from property investors is to be paid fortnightly rather than monthly by their property manager. The idea is to make better use of the rental income and have the money working for the investor, rather than sitting in the property manager's bank account.

What is the benefit in dollar terms? Is there a significant gain?

Finding Your Financial Ikigai: The Japanese Art of a Balanced & Purposeful Life

In a world that often measures success in financial terms, the Japanese concept of Ikigai offers a refreshing perspective. Transcending the boundaries of culture and geography, this philosophy loosely translates as "a reason for being". Ikigai is a convergence of what you love, what you're good at, what the world needs, and what you can be paid for. It's an approach that represents a broader view of prosperity, encompassing joy, purpose, and contentment. As financial advisers, we find this particularly compelling. This article delves deeper into how Ikigai can not only enrich your life but also inform your financial decisions for a more fulfilling journey.