Are interest rates heading back up to ‘normal’?

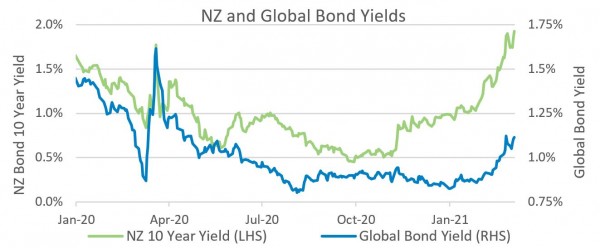

The Fixed Interest investments (or bonds) in portfolios typically perform well during market stress, as investors favour low-risk assets that generate income. Last year was no exception. High quality bonds benefitted from being seen as a ‘safe-haven’ asset during the Covid-19 uncertainty, and strong demand saw interest rates on long-term bonds (‘bond yields’) pushed down to historic lows - thanks partly to central banks buying huge amounts of them as part of their stimulus efforts. This in turn led to solid revaluation gains on the bonds in our funds, helping to support returns just when investors needed it most. Since then, bond yields have risen as economic data rebounds and with the rollout of vaccinations around the world.

Although long-term bond yields have recently gone up, they have simply gone back to where they were at the start of last year, pre-Covid. Importantly, central banks worldwide continue to hold their official short-term interest rates near zero to support the economic recovery. This should temper how much further longer-term interest rates might increase from here. However, if inflation does begin to rise above long-term targets, central banks will eventually come under more pressure to raise cash rates – even if that’s further off in the future.

Adding to the mix, in February the Reserve Bank was asked to include house price sustainability (and therefore house prices) more specifically in setting interest rates. While the Reserve Bank already consider house prices from a wider financial stability standpoint, the change puts more pressure on them to not ‘stoke the fire’ of the housing market any further. This makes it more likely that a negative Official Cash Rate (OCR) is now off the table.

Managing risks and opportunities

Booster's funds’ allocation to bonds acted as an important ‘shock absorber’ during last year’s share market sell-off. However, with historically low yields, the challenge became how to adapt your fixed interest investments as the outlook evolves. Booster have tackled this challenge in a few key ways, to best balance portfolios for the future across a range of scenarios.

Booster have sold some of the longer term bonds within Booster funds’ NZ and overseas fixed interest investments, crystalising some of the revaluation gains from the past year. They are keeping a close watch on the decision while temporarily keeping the proceeds in cash with a view to locking in better reinvestment rates in the future.

This follows adding some protection against a potential rise in inflation, by buying some US and NZ government inflation-linked bonds over the second half of 2020. Simply put, the interest payments on these bonds increase with inflation. So, they perform better than ‘normal’ when inflation rises, and underperform when it falls. This decision has already made a positive contribution as inflation has picked up; albeit remaining low at only 1.4%.

An important part of a diversified approach

Fixed interest investments remain an important part of Booster funds, but one that requires careful active management. Because most investment portfolios include both fixed interest and shares, the two normally work well together to capture growth while ‘smoothing the ride’ when markets receive an unexpected curve-ball, and this is an important dynamic to keep. This sits alongside the key direction within Booster funds over the past three years of expanding investments directly into businesses and land that deliver a sustainable income, which also directly address the challenge from today’s interest rates. Booster continue to actively pursue this direction across a range of investment areas, and we look forward to keeping you updated.

Disclaimer: This article has been prepared for the purpose of providing general information, without taking into consideration any particular investor’s objectives, financial situation or needs. Any opinions contained in it are held by the author as at the report date and are subject to change without notice.

KiwiSaver is changing

Budget 2025 has introduced some significant updates to KiwiSaver. These changes are aimed at ensuring the scheme remains sustainable while helping New Zealanders grow their retirement savings. Whether you are just starting out, nearing retirement, or somewhere in between, here's what you need to know and how it might affect your financial plans.

Lifetime Book Club: Four Thousand Weeks by Oliver Burkeman

In a world obsessed with productivity hacks, endless to-do lists and squeezing more out of every day, Burkeman offers something radical: acceptance. Not of defeat – but of reality. Because when you really look at it, four thousand weeks (roughly 80 years) is all we’ve got. And no app or bullet journal is going to give us more.